Sustainable: 2024 overview and outlook for 2025

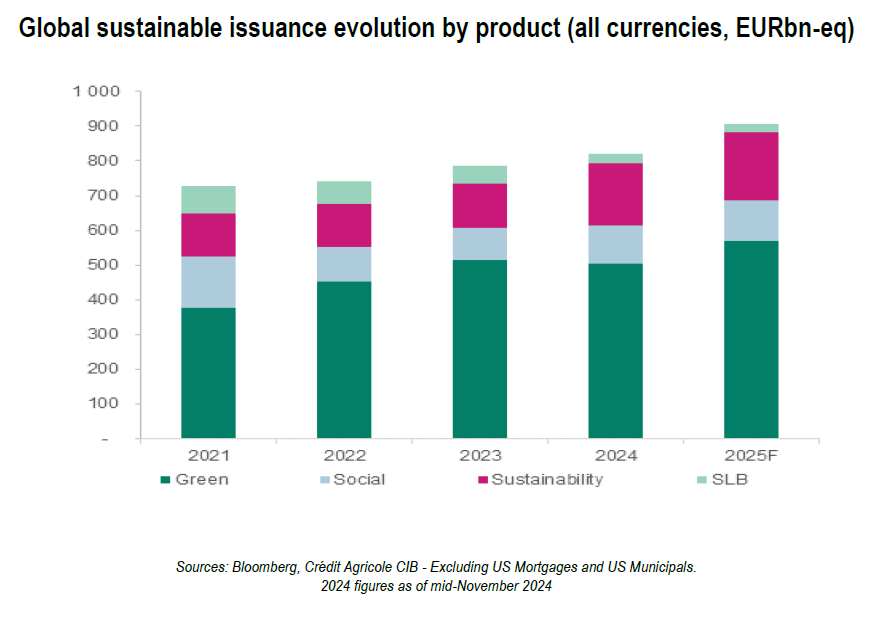

As the integration of environmental and social challenges continues, the volume of sustainable bond issuance is expected to reach c.EUR 900bn-eq in 2025, resulting in a c.10% growth vs 2024, according to Crédit Agricole CIB ESG Fixed Income Research team.

Given the current macroeconomic and geopolitical landscape, the momentum for ESG investments in 2025 may not be as strong as required for the transition to a low-carbon economy to stay within the 1.5°C scenario. However, over the longer term, ESG investments and sustainable finance will continue to have a disruptive impact on capital markets.

The challenging 2024 macro environment will continue to impact in 2025

Europe, a key engine in recent years in promoting the green transition, is now facing the dilemma between further decarbonization to meet its mid-term ambitions and reviving its industry competitiveness.

Such a difficult reconciliation comes amid political instability in several EU countries and expected rising protectionism pressures globally, which could have adverse impacts on the speed of the region's transition. For (European) Banks, growing prudential requirements under Basel III and Pillar 3 will increase further integration of climate and ESG risks in bank governance and risk appetite frameworks.

In the US, the recent outcome of the presidential election might be negative for the country's transition, with side-effects on Europe and other regions. In addition, intensifying trade tensions between the US and China can lead to higher levies towards Chinese clean technologies and products, creating supply chain disruptions and higher pressure for domestic industries to remain competitive internationally.

Soft ESG momentum led to a modest growth in the global sustainable bond market in 2024

In spite of a soft momentum around ESG investment in 2024, the sustainable bond market has slowly grown with around EUR 820bn-eq of sustainable bonds issued by mid-November, compared to EUR 790bn-eq in 2023. Green bonds have kept the lion’s share, representing 82.61% in 2024. The issuance has been mainly driven by supranationals and non-financials, which have issued 50% and respectively 20% more vs 2023.

Key drivers for a slow increase in the sustainable bond supply in 2025

Sustainable bond issuance should be marginally higher in 2025, driven by non-financials and supranationals.

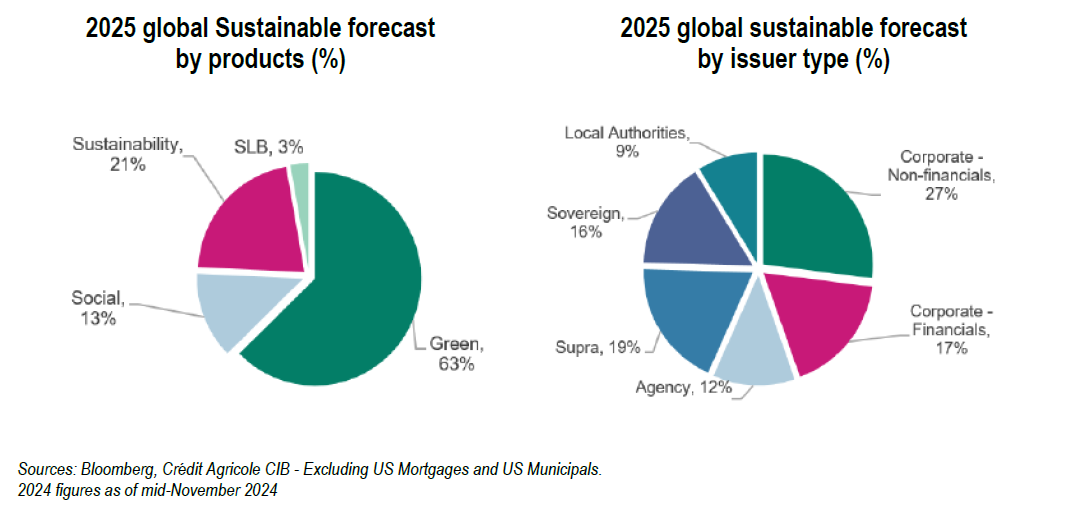

We expect the market to pursue its growth slowly but surely in 2025 to reach c.EUR 900bn-eq. with green bonds remaining the favourite product (c. 63% of the total) and SLBs should remain shy (only 3% of the expected volume ESG-labeled bond supply). The refinancing of upcoming maturing SLBs will be a key test for the segment, as pre-funding for SLBs maturing in 2026 and 2027 will start in 2025.

Green bonds will continue as the dominant product in 2025, although there will be some regional and product diversification. The coming into effect of the EU Green Bonds Standard (EU GBS) will be one of the main developments to follow in 2025, although Crédit Agricole CIB ESG Fixed Income Research team does not foresee a strong adoption at the beginning. The first impact on volumes will be clearer by 2026-2030.

Similar to 2024, we expect non-financials to have the highest share of sustainable bond issuance in 2025, with a slight year-on-year increase on an absolute basis. To generate a more robust supply, corporates will overall need clear regulatory and funding frameworks to support low-carbon technology scale-up.

ESG disclosures in Europe are expected continue to improve in 2025 both on the issuer and on the investor side, and this is likely to lead to better ESG data comparability and transparency around how ESG risks affect capital markets in the long run.

“Amid geopolitical uncertainties and despite growing concerns on public deficits in many regions, energy transition should remain on top of the agenda for many investors and corporates, hence still supporting growth in the sustainable bond market. However, finding the balance between competitiveness and sustainable targets has become a growing topic across sectors and geographies. Regulation, particularly in Europe, will continue to play a key role especially as the carbon border levy (CBAM) will take place in 2026. In turn, we expect green capex to accelerate in hard-to-abate sectors. In the credit market, as greenium has continued to reduce with investors’ focus skewed onto yield, more disclosures (CSRD) should pave the way for more differentiation between leaders and laggards. In that respect, 2025 is set to be a key milestone in assessing the credibility of the green trajectories embedded in 2030 sustainable targets.”

Damien de Saint Germain

Head of Credit Research & Strategy at Crédit Agricole CIB

- EnglishPDF288.44 KBRead the press releaseRead the press release

- Sustainable financeArticle11/06/2026

Climate adaptation conference: from physical risks to adaptation finance

- StrategyArticle22/05/2026

Crédit Agricole CIB launches Optimtrade, its new digital trade finance portal to enhance its corporate clients' experience worldwide

- StrategyPress Release30/04/2026

Financial results for the first quarter 2026